How Long Does the VA Loan Process Take?

Getting

a VA loan can help military families buy their dream

home. The VA loan process offers unique benefits that

conventional loan options don't provide. Many veterans

want to know precisely how long it takes to get a VA

loan approved and closed.

Getting

a VA loan can help military families buy their dream

home. The VA loan process offers unique benefits that

conventional loan options don't provide. Many veterans

want to know precisely how long it takes to get a VA

loan approved and closed.

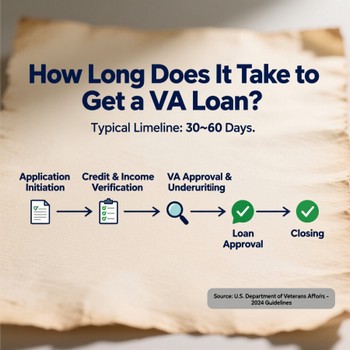

The timeline for VA loan approval depends on several factors. Most borrowers can expect the process to take 30 to 45 days from application to closing, especially when working with a VA lender. However, some cases may take longer depending on market conditions and your specific situation.

Try our funding fee calculator

Understanding the VA Home Loan Timeline

The VA home loan process involves multiple steps that each take time to complete. When you apply for a VA loan, you start a process that includes several key phases. Each step has its own timeline, which affects the overall process duration.

Your lender plays a significant role in determining how quickly your loan moves forward. Some lenders process VA loan applications faster than others. The housing market conditions in your area also impact the timeline.

Getting preapproved for a VA loan is the first significant step. This process typically takes 1 to 3 days if you have all the required documents ready, which is essential for those eligible for a VA loan. Prequalified borrowers often move through the process more smoothly.

Certificate of Eligibility Requirements

Before you can get a VA loan, you need your certificate of eligibility. This document confirms that you qualify for VA loan benefits. The VA issues this certificate to eligible veterans, service members, and surviving spouses.

You can apply for your loan certificate of eligibility online through the VA's eBenefits portal. Most applications receive approval within days. Some cases may take longer if additional documentation is needed.

Having your certificate of eligibility ready before you start home shopping saves time. Many veterans get this document early in their home-buying journey. This preparation helps speed up the overall VA loan process.

VA Loan Approval Timeline

The VA loan approval process involves several necessary steps. After you submit your application, your lender begins reviewing your financial information. This initial review typically takes 3 to 5 business days.

Your credit score, income, and debt-to-income ratio all impact the timing of approval. Borrowers with firm financial profiles often get approved faster. Those with complex financial situations may need additional time for underwriting.

The underwriter examines your application in detail during this phase. They verify your income, employment, and financial assets. This step usually takes 1 to 2 weeks to complete, depending on how long it takes to meet the minimum property requirements.

VA Appraisal Process and Timeline

Every VA home loan requires a VA appraisal to determine the property's value and ensure it meets minimum property requirements. The VA assigns a VA appraiser to inspect the home and assess its condition. This appraisal protects both you and the VA from overpaying.

Scheduling the VA appraisal can take 1 to 2 weeks, depending on your local market. Busy housing markets may have longer wait times for appraisers. Rural areas might also experience delays due to fewer available appraisers.

The actual appraisal inspection takes a few hours to complete. The VA appraiser then has up to 10 business days to submit their report. Most appraisals are completed within this timeframe.

Factors That Affect VA Loan Processing Time

Several factors determine how long a VA loan takes to close. Market conditions play a significant role in timing, which can affect how long it takes to close on a VA loan. Hot housing markets with lots of activity can slow down the process.

Your lender's workload affects processing speed. During busy seasons, lenders may take longer to review applications. Choosing an experienced VA-approved lender can help speed things up.

Your financial situation impacts timing as well. Clean credit reports and stable income help the loan process run faster. Issues with employment verification or unusual income sources can take longer to review.

The property you want to buy also affects timing. Homes that need repairs may require additional appraisal work. This can add weeks to your timeline.

Loan Closing Timeline and Final Steps

Once your VA loan approval is complete, you move toward closing. The loan closing process typically takes 1 to 2 weeks to finalize. During this time, your lender prepares all final documents.

You'll receive a Closing Disclosure at least three days before closing, which is crucial for a smooth VA loan closing process. This document outlines your final loan terms and closing costs. Review this carefully to make sure everything is correct.

The actual closing appointment usually takes 1 to 2 hours. You'll sign numerous documents and receive your keys. After closing, your loan moves to servicing for monthly payment processing.

Ways to Speed Up Your VA Loan Process

Getting prequalified early helps speed up the entire process. This shows sellers you're a serious buyer with financing lined up. Many real estate agents prefer working with prequalified buyers.

Gather all required documents before you apply. Your lender needs pay stubs, tax returns, bank statements, and military records. Having these ready prevents delays.

Choose an experienced VA mortgage lender who knows the process well. These lenders understand VA loan requirements and can avoid common mistakes. They have also established relationships with VA appraisers.

Stay in close contact with your lender throughout the process. Respond quickly to any requests for additional information to ensure that you remain eligible for a VA loan. This keeps your application moving forward without unnecessary delays.

VA Loan Benefits That Make the Wait Worth It

VA loan benefits make the longer timeline worthwhile for many military families. You don't need a down payment with most VA loans. This saves thousands of dollars upfront, making home buying more accessible for those eligible for a VA loan.

VA loans don't require private mortgage insurance (PMI). This saves you hundreds of dollars each month compared to conventional loan options. The savings add up to thousands over the life of your loan.

Interest rates on VA home loans are generally lower than those on other mortgage options. This lower rate saves money on your monthly payment and total interest paid.

You can refinance your VA loan later if rates drop, providing additional flexibility for active duty members. The VA offers streamlined refinance options that simplify the process for those who are already eligible for a VA loan. This flexibility helps you save money over time, making it easier to qualify for a VA loan.

Planning Your Home Purchase Timeline

Start your VA loan process early when you decide to buy a home. Getting your certificate of eligibility and prequalification done first saves time later. This preparation helps you move quickly when you find the right home.

Work with a real estate agent experienced with VA loans. These agents understand the process and can help set realistic expectations. They also know how to write competitive offers that work with VA loan timelines.

Plan for potential delays when making your offer. Include reasonable timeframes in your purchase contract. This protects you if the process takes longer than expected.

VA Loan Approval Timeline

The VA loan approval timeline varies based on multiple factors, but most borrowers complete the process within 30 to 45 days. Understanding each step helps you prepare and set realistic expectations for your home purchase, especially regarding VA loan closing timelines.

Initial Application and Documentation

When you apply for a VA loan, your lender begins the approval process immediately. They collect your financial documents and verify your information. This initial step typically takes 3 to 5 business days to complete.

Your lender checks your credit score, income, and employment history. They also verify your VA loan eligibility through your military service records. Having all documents ready speeds up this process significantly.

Underwriting and Final Approval

The underwriting process is where your lender takes a detailed look at your financial profile. An underwriter reviews your application to ensure you meet all VA loan requirements. This step usually takes 1 to 2 weeks.

During underwriting, your lender may request additional documents or clarification. Responding quickly to these requests keeps your application on track. Most borrowers get approved for a VA loan during this phase.

Certificate of Eligibility

Your certificate of eligibility is the foundation of your VA loan application. This document proves you qualify for VA loan benefits based on your military service. Getting this certificate early in the process saves time later.

How to Get Your Certificate

You can apply for your certificate online, by mail, or through your lender. The online eBenefits portal is usually the fastest option. Most applications receive approval within a few business days, particularly if they meet the Department of Veterans Affairs requirements.

Your lender can also assist you in obtaining your certificate of eligibility. Many VA mortgage lenders can pull this information directly from VA systems. This service can speed up your application process.

Using Your Certificate for Multiple Purchases

Your certificate of eligibility doesn't expire and can be used for multiple home purchases. You can buy, sell, and buy again using your VA loan benefits. The VA tracks your usage through this certificate.

If you've used your VA loan benefits before, you might have remaining eligibility. The certificate indicates the amount of your benefit that is available. Most veterans can restore their full eligibility after paying off previous VA loans, which allows them to qualify for a VA loan again.

Connect With Us

Please share – it really helps