How Many Times Can You Use a VA Loan?

The VA home loan program is a fantastic resource for eligible

veterans, active-duty service members, and surviving spouses looking

to buy property. One common question among those interested in using

this benefit is, "How many times can you use a VA home loan?"

The VA home loan program is a fantastic resource for eligible

veterans, active-duty service members, and surviving spouses looking

to buy property. One common question among those interested in using

this benefit is, "How many times can you use a VA home loan?"

The answer is encouraging: you can use your VA loan benefit many

times throughout your life. Understanding the nuances of VA

entitlement is key to maximizing this valuable resource.

Understanding VA Loan Entitlement

To fully understand how many times you can access this program,

it's important to grasp the concept of entitlement. The Department

of Veterans Affairs (VA) guarantees a portion of your mortgage,

protecting the lender if you default.

This guarantee is

what's known as your entitlement, and it makes it easier for

veterans to secure financing with favorable terms, often with no

down payment.

What is VA Loan Entitlement?

Entitlement is the amount the VA guarantees to a lender when you buy property through this program. There are generally two types to be aware of:

- Basic entitlement: This is a standard amount available to all eligible veterans, allowing them to access their VA loan benefit.

- Bonus or additional entitlement: This allows veterans to borrow more without needing a down payment, enhancing their ability to use their VA loan benefit.

The amount of entitlement you have can influence the loan amount you're able to secure.

How Entitlement Affects Your VA Loan

Your entitlement plays a major role in determining how much you

can borrow when you use your VA loan benefit. Lenders consider your

entitlement when assessing your application.

If you have full

entitlement, you are generally eligible for a larger loan amount,

often up to the current loan limit, without needing a down payment.

But if you've used some of your entitlement, your remaining benefits

will affect how much you can buy.

Managing your borrowing

power wisely is important for future home purchases.

Restoring Your VA Loan Entitlement

If you've used this benefit before and want to buy another home,

you may be wondering how to reuse it. Even if you have a mortgage

through the program, you can restore it and get a VA loan to secure

new financing.

There are a few ways to restore your

entitlement and use your VA loan benefits, allowing you to access

them again. One common method is to pay off the mortgage in full and

sell the property.

This restores your entitlement to its

original amount, making you eligible for additional financing.

Using a VA Loan Multiple Times

This program's biggest benefit is that you can use it many times

in your life. Unlike some other loan programs that limit you to a

single use, the VA understands that veterans may need to buy a home

more than once due to changing life circumstances, such as

relocation for work or family needs.

The ability to reuse

your entitlement provides considerable flexibility and financial

advantages for eligible veterans. Learning how many times you can

access this financing is key for maximizing your benefits.

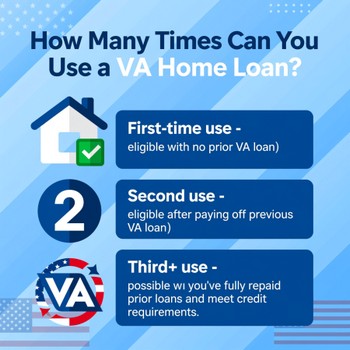

How Many Times Can You Use a VA Loan?

This question often arises, and the answer is reassuring: there

is no limit to the number of times you can use your VA benefits. The

key factor determining your eligibility for buying another property

is your remaining entitlement.

If you have full entitlement

available, you can apply for new financing and get a VA loan. If

you've used your benefits before and haven't fully restored your

entitlement, you may still be able to use your remaining borrowing

power to buy property, but it might affect the amount you can

secure.

The VA makes it possible to access this program many

times you can use it throughout your life.

Applying for a New VA Loan

The lender will assess your entitlement to determine your

eligibility and the amount you qualify for. If you have full

entitlement, the process is generally straightforward.

If

you've used some of your VA entitlement, the lender will calculate

your remaining benefits and factor that into the approval process.

This might involve looking at the loan limit for your area and any

outstanding mortgages you may have.

Understanding the

requirements and how your entitlement balance affects your options

is helpful when applying for new financing to get a VA loan.

Conditions for Taking Out a Second VA Loan

While you can use this benefit multiple times, there are

conditions that must be met to take out a second mortgage,

especially if you still have an existing one. One common scenario is

using your remaining entitlement to acquire another property while

still paying off the previous mortgage.

In this case, the VA

will assess your debt-to-income ratio and your ability to manage

both mortgages. Alternatively, you can restore your full entitlement

by selling your current home and paying off the mortgage in full,

which may help you avoid the VA funding fee.

This allows you

to apply for new financing with full entitlement, essentially

resetting your benefits. The funding fee is also a factor to

consider.

VA Home Loan Benefits

Loan Benefits of a VA Home Loan

These VA loans offer numerous advantages to eligible veterans, making homeownership more accessible. These benefits include the ability to get a VA loan and potentially reduce your interest rate through a refinance loan that lowers your interest rate.

- These loans offer the potential for no down payment, enabling veterans to purchase a property without requiring a substantial upfront investment.

- Interest rates that tend to be lower than conventional mortgage rates, resulting in significant long-term savings.

The VA also provides support and resources to help veterans navigate the home buying process, ensuring they can use their benefits effectively. The program helps veterans buy homes using their VA benefits.

VA Mortgage vs. Conventional Loans

When comparing this financing option to conventional loans,

several key differences stand out. These mortgages typically do not

require private mortgage insurance (PMI), which can save borrowers

hundreds of dollars each month.

Conventional loans, on the

other hand, often require PMI if the borrower makes a down payment

of less than 20%. Furthermore, qualification requirements are often

more lenient, making it easier for veterans to qualify.

These

differences make this program an attractive option for veterans

looking to purchase a home or refinance. You can access this

financing multiple times throughout your life.

Understanding Your VA Home Loan Benefit

Understanding your benefits is helpful for maximizing their

value. The program is designed to help veterans buy a home with

favorable terms, and knowing the ins and outs can save you money and

stress.

Familiarize yourself with the entitlement, loan

limits, and eligibility requirements. You can also explore resources

provided by the VA to learn more about your benefits and how to use

them effectively.

Having a solid understanding of the VA

entitlement program is valuable for veterans.

Practical Steps to Use Your VA Loan

How to Apply for a VA Loan

To apply, there are a few key steps you'll need to follow to use your VA loan benefit effectively. Veterans can apply many times; they can use it throughout their lives for new loans. These steps include:

- Obtaining a Certificate of Eligibility (COE) from the VA, proving you're eligible for this VA loan benefit, is essential to accessing your VA loan in full.

- Finding a lender and completing an application, providing necessary documentation, such as proof of income and credit history.

The lender will then assess your eligibility and determine the amount you qualify for.

Using Your VA Loan for a Second Home

Using this benefit for a second home is possible, although it's

subject to certain conditions. Generally, the program is designed

for primary residences, so you'll need to demonstrate that you

intend to occupy the new property as your main home to use VA

benefits.

If you have remaining entitlement, you may be able

to purchase a second home while still owning your current home.

However, the VA will assess your ability to manage both mortgages.

You can still access this financing to acquire property with

your VA loan benefit.

Managing Two VA Loans at the Same Time

Managing two mortgages through this program at the same time can

be complex but is achievable under specific circumstances when you

reuse your VA loan. The VA will assess your debt-to-income ratio and

creditworthiness to ensure you can handle the financial burden of

two mortgages while utilizing your VA funding.

If you have

sufficient remaining entitlement and meet the VA's requirements, you

may be able to secure a second mortgage while still paying off the

previous one. Proper budgeting and financial planning are necessary

when managing two mortgages at the same time.

You can use

this benefit multiple times when you meet the requirements.

Connect With Us

Please share – it really helps