VA Loan Eligibility Requirements

The

VA loan

program offers qualified military members and veterans an

opportunity to purchase a home with no down payment and competitive

rates. Understanding the eligibility requirements helps

service members determine if they qualify for this valuable benefit.

The

VA loan

program offers qualified military members and veterans an

opportunity to purchase a home with no down payment and competitive

rates. Understanding the eligibility requirements helps

service members determine if they qualify for this valuable benefit.

What is a VA Loan Program?

The Department of Veterans Affairs created the VA loan program to help military members achieve homeownership. This loan benefit provides veterans, active-duty service members, and eligible spouses with access to home financing on favorable terms. The VA backs these loans, reducing risk for lenders and creating better conditions for borrowers seeking a VA mortgage.

VA loans offer several advantages over conventional home loans, including lower interest rates and no down payment. Borrowers can purchase a home without a down payment in most cases. The program also eliminates private mortgage insurance requirements, saving money each month. Veterans can refinance existing loans through VA programs and may qualify for special adapted housing grants, which can help them buy a home.

Basic Service Requirements for VA Loan Eligibility

Active Duty Military Members

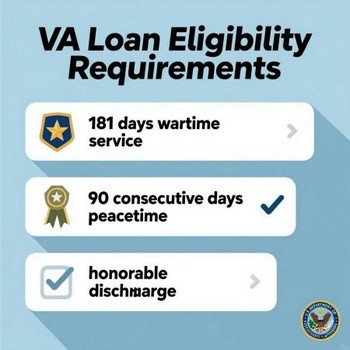

Current military personnel become eligible for a VA loan after serving 90 consecutive days of wartime service or 181 days of peacetime service. Each branch of the military has members who can apply for this loan benefit. The Army, Navy, Air Force, Marine Corps, Coast Guard, and Space Force all participate in the program.

Active duty members can apply for a VA loan while still serving. They do not need to wait until retirement or separation to access this benefit. Military personnel can use the loan multiple times throughout their service and after separation.

Veterans and Former Service Members

Veterans who received an honorable discharge qualify for VA loan benefits. The length of service determines eligibility. Veterans who served during wartime require at least 90 days of active duty service. Those who served during peacetime require 181 days of continuous active duty service.

Some veterans with shorter service periods may still qualify. Those discharged for a service-connected disability may be eligible for a VA mortgage, regardless of their service length. Veterans with hardship discharges may also be eligible under certain conditions.

National Guard and Reserve Members

National Guard and Reserve members have specific eligibility requirements. They must complete six years of service to qualify for a VA loan. Members who served on active duty for at least 90 days during a period of war also meet the requirements. Reserve and National Guard personnel called to active duty under federal orders may qualify with shorter service periods.

The VA recognizes service in the Army National Guard, Air National Guard, Army Reserve, Navy Reserve, Marine Corps Reserve, Air Force Reserve, and Coast Guard Reserve. Each component has members eligible for loan benefits after meeting service requirements.

Surviving Spouses

Surviving spouses of veterans may qualify for VA loan benefits under specific circumstances. The veteran spouse must have died in service or from a service-connected disability. Some surviving spouses who remarried after age 57 can retain eligibility for a VA home loan. Spouses of prisoners of war or those missing in action may also qualify.

The VA reviews each case individually to determine eligibility as a surviving spouse. Required documentation includes death certificates and proof of the veteran's service record.

Certificate of Eligibility Requirements

Obtaining Your COE

The Certificate of Eligibility (COE) proves your qualification for a VA loan. Veterans and service members must obtain this certificate before applying for financing. The VA issues the COE after verifying military service and discharge status.

Applicants can request a COE through several methods. The eBenefits portal allows online applications, resulting in faster processing. Veterans can also apply by mail using VA Form 26-1880. Lenders often help borrowers obtain the COE during the loan application process.

Required Documentation for COE

The COE application requires specific military documents. Veterans need their DD-214 discharge papers, which show their service dates and discharge type. Active duty members provide a statement of service from their commanding officer.

National Guard and Reserve members need additional documentation. They must provide their latest annual retirement points statement and evidence of honorable service. The VA may request additional records to verify eligibility.

COE Processing Time

Standard COE applications typically process within 2-3 weeks. Online applications through eBenefits often receive faster processing - veterans with complete documentation experience shorter wait times.

Some applications require additional review and take longer to process. Complex cases involving disability discharges or surviving-spouse claims may require additional time. The VA contacts applicants if they need further information.

Financial and Credit Requirements

Minimum Credit Score Considerations

VA loans do not have a government-mandated minimum credit score. However, most lenders require credit scores of 580 or higher. Some lenders may accept lower scores with additional documentation or larger down payments.

Veterans with credit challenges have options. They can work with VA-approved lenders who specialize in helping borrowers with lower credit scores. Credit counseling and debt consolidation may help improve scores before applying.

Income and Employment Verification

Borrowers must demonstrate stable income to qualify for a VA loan. Lenders verify employment history and current income through pay stubs, tax returns, and employment letters. Military members can utilize their base pay, allowances, and other forms of military income.

The VA does not set specific income requirements. Instead, lenders evaluate debt-to-income ratios to determine affordability. Most lenders prefer ratios below 41%, though exceptions exist for well-qualified borrowers.

VA Funding Fee

Most VA loan borrowers pay a funding fee to support the program. The cost varies based on loan type, down payment amount, and veteran status. First-time users typically pay 2.15% of the loan amount. Veterans using the benefit again pay 3.3%.

Some veterans are exempt from the funding fee. Those receiving VA disability compensation do not pay this fee. Surviving spouses also receive funding fee exemptions in most cases when applying for a VA home loan.

Try our funding fee Calculator

Property Requirements and Restrictions

Primary Residence Requirement

VA loans can only finance primary residences. Borrowers must occupy the home within 60 days of closing. The property cannot be used solely as an investment or vacation home.

Veterans can purchase various property types with VA loans. Single-family homes, condominiums, and manufactured homes are all eligible. Multi-unit properties up to four units are allowed if the borrower lives in one unit.

Property Condition Standards

VA loans require properties to meet minimum condition standards. The home must be safe, structurally sound, and sanitary. VA appraisers inspect properties to verify they meet these requirements.

Properties with significant defects may not qualify. Issues like faulty electrical systems, plumbing problems, or structural damage must be repaired before loan approval. The VA protects borrowers by ensuring properties are suitable for occupancy.

Types of VA Loans Available

Purchase Loans

VA purchase loans help veterans buy homes with favorable terms. These loans offer 100% financing for qualified borrowers. Veterans can purchase homes without down payments in most cases.

The loan amount for a VA mortgage depends on the VA loan limit in the area. Veterans with full entitlement can borrow up to the conforming loan limit without down payments. Those with reduced entitlement may need a larger down payment for higher-priced homes.

Refinance Options

Veterans can refinance existing loans through VA programs. The Interest Rate Reduction Refinance Loan (IRRRL) helps veterans lower their payments. This streamlined refinance typically requires minimal documentation and often no appraisal.

Cash-out refinancing enables veterans to tap into their home equity. This option requires a new appraisal and complete income verification. Veterans can use cash from refinancing a home for any purpose, including paying off debts or making home improvements.

Finding a VA-Approved Lender

Choosing the Right Lender

Not all mortgage companies offer VA loans. Veterans should find lenders approved by the VA to originate these loans. These lenders understand the program requirements and can guide borrowers through the process.

Veterans can compare offers from multiple lenders. Interest rates, closing costs, and service quality vary between lenders. Shopping around helps veterans find the best deal for their situation.

Working with Your Lender

Experienced VA lenders provide valuable guidance throughout the loan process. They help veterans gather the required documents and navigate the VA loan requirements. Good lenders educate borrowers about VA loan benefits, restrictions, and requirements.

Lenders also coordinate with the VA during the approval process. They order required appraisals and handle paperwork submissions. Veterans should maintain regular contact with their lender to ensure smooth processing.

Benefits of VA Loan Ownership

Financial Advantages

VA loans offer significant financial benefits compared to conventional financing. The no-down-payment feature helps veterans buy homes sooner. Eliminating private mortgage insurance saves hundreds of dollars monthly.

VA loans typically offer competitive interest rates. Government backing reduces lenders' risk, resulting in better rates for borrowers. Veterans also pay lower closing costs through VA regulations.

Long-term Value

Homeownership builds wealth over time through appreciation and equity. Veterans using VA loans start building equity immediately without down payments. The stable housing costs help families budget effectively.

VA loan benefits extend beyond the initial purchase, allowing veterans to refinance a home later. Veterans can use the benefit multiple times throughout their lives. The program supports the housing needs of military families during service and retirement.

Steps to Apply for Your VA Loan

Veterans ready to apply should start by obtaining their COE. This certificate proves eligibility and speeds up the loan process. Online applications through eBenefits offer the fastest processing.

Next, veterans should research and contact VA-approved lenders. Comparing offers from multiple lenders helps find the best terms. Pre-approval letters demonstrate serious intent to sellers.

The home shopping process follows pre-approval. Veterans should work with real estate agents familiar with VA loans. These agents understand program requirements and can identify suitable properties.

After finding a home, the formal loan application begins. Lenders verify income, assets, and creditworthiness. The VA orders an appraisal to ensure the property meets program standards.

Closing typically occurs 30 to 45 days after contract acceptance. Veterans review all loan documents and sign final paperwork. The lender funds the loan, and veterans receive their keys.

The VA loan program represents a valuable benefit for those who served our nation. Understanding eligibility requirements helps veterans access this program and achieve homeownership goals. Veterans should explore this benefit to determine if VA financing fits their needs.

Connect With Us

Please share – it really helps