VA Loan Amount Limit

The

Department of Veterans Affairs sets specific limits on how much

veterans can borrow through VA loans each year. These 2026 VA loan

limits determine the maximum amount you can borrow without making a

down payment under the VA guarantees. VA loans offer qualified

veterans, active-duty service members, and eligible spouses the

opportunity to buy a home with favorable terms and no down payment

requirements.

The

Department of Veterans Affairs sets specific limits on how much

veterans can borrow through VA loans each year. These 2026 VA loan

limits determine the maximum amount you can borrow without making a

down payment under the VA guarantees. VA loans offer qualified

veterans, active-duty service members, and eligible spouses the

opportunity to buy a home with favorable terms and no down payment

requirements.

VA loan limits vary by county and reflect local housing costs, which in turn affect VA guarantees. The baseline serves as the foundation for most areas, while high-cost counties receive higher limits. Understanding these limits helps veterans plan their home purchases and maximize their benefits.

The 2026 VA loan limits apply differently depending on your status and location. Veterans with full access can often borrow more than the published limits, while those with partial access face stricter constraints. Your loan amount depends on several factors, including your status, the county loan limit, and your ability to qualify for the mortgage.

How VA Loan Limits Work in Practice

VA loans operate through a guarantee system in which the VA guarantees a portion of your loan to the lender. This guarantee eliminates the need for private mortgage insurance and often allows veterans to get a VA loan without making a down payment. The loan limit represents the maximum amount the VA will guarantee in a specific county, influencing the full VA entitlement.

Basic Entitlement and How It Affects Your Loan

Every eligible veteran starts with basic access of $36,000 in VA loan entitlement. This amount represents the foundation of your benefit and stays with you throughout your military service and beyond. The basic access allows you to borrow up to $144,000 in most areas without a down payment, though few homes cost this little in today's market.

Your total access includes the basic amount plus additional amounts based on the county loan limit for the county where you plan to buy a home. The additional access bridges the gap between the basic amount and the full loan amount available through VA loan programs.

Key access facts include:

- Basic access remains constant at $36,000 for all eligible veterans

- Additional access varies by county and changes annually with new limits

- Total access equals basic plus additional amounts

- Veterans can restore access after paying off a prior loan • Remaining access carries forward to future home purchases

2026 VA Loan Limit Changes and Updates

The 2026 loan limits reflect current housing market conditions and follow the baseline set by the Federal Housing Finance Agency. Most counties will see the baseline of $806,500, representing an increase from previous years. High-cost areas receive higher limits based on median home values and local market conditions.

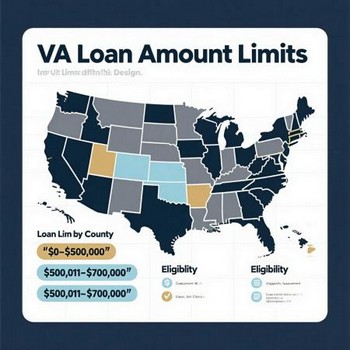

County-Specific Limits Across the United States

VA loan limits by county vary significantly across different regions. Urban areas and high-cost markets typically receive the highest VA home loan limits, while rural areas often use the baseline. Veterans should check their specific county loan limit before starting their home search to understand their borrowing capacity.

The county loan system recognizes that housing costs vary widely across locations, which affects VA home loan limits. A veteran in San Francisco faces different market conditions than someone buying in rural Kansas. The VA adjusts limits accordingly to ensure veterans can access homeownership opportunities regardless of where they choose to live.

Examples of how limits vary:

- Baseline counties: $806,500 (most areas across the United States)

- High-cost markets: Up to $1,149,825 in the most expensive counties

- Hawaii and Alaska: Special consideration for unique market conditions

- Military housing areas: Often receive elevated limits due to base proximity

- Rural markets: Typically follow the baseline

Understanding Your Borrowing Power with VA Entitlement

Veterans with full entitlement can often borrow more than the published VA loan limit without making a down payment. Full entitlement means you have never used VA loans before, or you have paid off a prior loan and restored your entitlement. This status provides maximum flexibility when choosing a home and loan amount under the VA home loan limits.

Full Entitlement vs Partial Entitlement Benefits

Full entitlement holders can typically borrow up to four times their total entitlement without a down payment. Since the 2026 VA loan limits set the baseline at $806,500 in most areas, veterans with full entitlement may be able to borrow more than that amount in many situations. The exact amount depends on your income, credit score, and ability to qualify for the mortgage payment.

Partial entitlement occurs when you have used your VA loan benefit before but still have remaining entitlement available. Veterans in this situation can still get VA loans, but their borrowing capacity depends on how much entitlement remains unused. The amount you can borrow equals your remaining entitlement multiplied by four, up to the county loan limit.

Entitlement restoration allows veterans to regain their full entitlement after paying off a prior loan. You can restore your VA loan entitlement by selling the home and paying off the loan, or by having another qualified veteran assume your previous VA loan. Restoration restores your full entitlement status for future home purchases.

Maximizing Your VA Home Loan Benefit

Understanding loan limits helps veterans make informed decisions about their home purchase. Veterans can buy homes above the VA loan limit by making a down payment on the amount exceeding the limit. For example, if the county loan limit is $806,500 but you want to buy an $850,000 home, you would need to make a down payment of $83,450.

VA loans offer several advantages beyond the loan amount benefits. Veterans avoid private mortgage insurance regardless of their down payment amount. The VA funding fee, while required in most cases, can be financed into the loan amount rather than paid up front. Veterans also benefit from competitive interest rates and flexible qualification requirements. Try our funding fee calculator

Multiple VA loans can be used simultaneously if you have sufficient VA loan entitlement. Veterans who move frequently for military assignments can keep their first home as a rental property while using the remaining entitlement for a new primary residence. This strategy helps build wealth through real estate investment while maintaining access to home loans and VA loans benefits.

Strategic considerations for maximizing benefits:

- Check your local county loan before starting your home search

- Consider the total cost of homeownership beyond the mortgage payment

- Evaluate whether to make a down payment for homes above the limit

- Plan for the VA funding fee in your loan calculations

- Research interest rates and shop with multiple approved lenders for VA loans

Taking the Next Steps with Your VA Loan Application

Veterans ready to use their benefits should obtain a Certificate of Eligibility from the Department of Veterans Affairs. This document confirms your entitlement amount and eligibility status. You can apply online through the VA website or work with an approved lender to obtain the certificate.

Choosing the right lender makes a significant difference in your experience. Look for lenders experienced with VA loans who understand the unique aspects of VA financing. Many lenders specialize in home loans and can guide you through the process more efficiently than general mortgage companies.

Pre-approval helps you understand exactly how much you can borrow based on your income, credit score, and entitlement. The process also identifies any issues that need to be resolved before you start shopping for homes. Veterans should get pre-approved before making offers to strengthen their negotiating position with sellers.

Connect With Us

Please share – it really helps