VA Mortgage Interest Rates Today

VA

mortgage interest rates

continue shifting in today's market, creating both opportunities and

challenges for eligible borrowers. The Department of Veterans

Affairs backs these special home loan programs, making homeownership

more accessible for those who served our country. Current market

conditions affect how lenders price these loan products, influencing

monthly payments

and overall borrowing costs for military families.

VA

mortgage interest rates

continue shifting in today's market, creating both opportunities and

challenges for eligible borrowers. The Department of Veterans

Affairs backs these special home loan programs, making homeownership

more accessible for those who served our country. Current market

conditions affect how lenders price these loan products, influencing

monthly payments

and overall borrowing costs for military families.

Understanding today's rate environment helps service members make informed decisions about when to take out a home loan. Multiple factors drive interest rate movements, including Federal Reserve policy, economic indicators, and housing market conditions. VA loan rates typically track closely with conventional mortgage rates, though they often offer slightly better terms due to government backing.

Lenders adjust their pricing daily based on market conditions and investor demand for mortgage-backed securities. This dynamic environment means borrowers should monitor rates regularly and act quickly when favorable conditions emerge. The VA loan program provides unique advantages that remain valuable regardless of current fluctuations in the broader mortgage market's interest rates.

Service members benefit from exclusive mortgage opportunities through the VA loan program. These government-backed loans offer competitive rates without requiring private mortgage insurance or down payments. The Department of Veterans Affairs guarantees a portion of each loan, reducing lender risk and enabling better terms for qualified borrowers seeking homeownership.

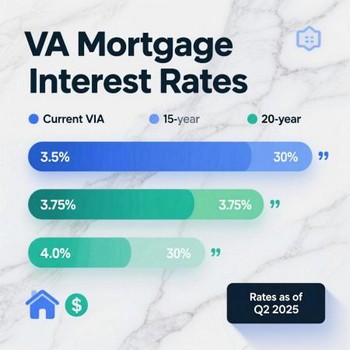

Current VA Loan Rate Trends and Market Analysis

Today's VA mortgage rates reflect broader economic trends affecting all loan types across the marketplace. Recent Federal Reserve decisions affect short-term rates, which in turn influence long-term mortgage pricing for all borrowers. Economic data releases, inflation reports, and employment statistics all contribute to daily rate movements that significantly affect home loan costs.

VA loan rates today typically vary based on loan type, borrower creditworthiness, and chosen loan terms. Purchase loans often carry different pricing than refinance loans, with cash-out refinance options sometimes commanding slightly higher rates. Lenders evaluate each application individually, carefully considering credit score, income stability, and debt-to-income ratio.

Try our debt-to-income calculator.

Market volatility creates opportunities for savvy borrowers who understand timing strategies and market patterns. Rate locks protect approved borrowers from unfavorable movements during the loan processing period, ensuring they benefit from today's mortgage rates. Most lenders offer 30-60 day lock periods, with extensions available for longer closing timelines when needed.

Key Rate Factors Affecting Your Loan Today

Several elements determine the specific interest rate each borrower receives:

- Credit score requirements vary by lender, though VA loans accommodate lower scores than conventional options

- Loan amount affects pricing, with jumbo loans often carrying higher rates than conforming loan limits

- Chosen loan term impacts rates, with 15-year mortgages typically offering lower rates than 30-year options

Current mortgage-rate environments favor borrowers with strong financial profiles and stable employment histories. Higher credit scores, stable employment, and lower debt-to-income ratios help secure the best available rates from lenders, particularly for a fixed-rate mortgage loan. VA loan benefits remain consistent regardless of market conditions, providing long-term value beyond just rate considerations for military families.

Regional differences affect local market pricing, as some areas command premium pricing due to higher default risks or limited lender competition. Online lenders often offer competitive rates by reducing overhead costs, while local banks provide personalized service and community knowledge. Shopping multiple loan options helps borrowers find the best terms available.

VA Home Loan Benefits That Go Beyond Interest Rates

VA home loans provide advantages that extend far beyond competitive mortgage rates. The loan program eliminates the requirement for private mortgage insurance, saving borrowers hundreds of dollars per month compared to conventional financing options. This benefit alone can offset slightly higher interest rates when they occur, making the monthly mortgage payment more manageable.

Zero-down payment requirements make homeownership accessible to service members without substantial savings for traditional mortgages. Conventional loans typically require 5-20% down payments, creating significant barriers for many potential buyers in today's market. VA loans remove this major obstacle, allowing eligible borrowers to finance 100% of the home purchase price.

Flexible credit score requirements accommodate borrowers who might struggle with conventional loan approval processes. While individual lenders set their own underwriting standards, VA loans generally accept lower credit scores than traditional mortgage products. This flexibility helps more service members achieve homeownership goals despite past financial challenges.

The VA loan benefit extends to refinancing options that help borrowers optimize their mortgage terms over time as rates change. Interest Rate Reduction Refinance Loans (IRRRL) streamline the refinancing process, often requiring minimal documentation and no new appraisal. These refinanced loans help borrowers lower their monthly payments or adjust their loan terms as market conditions change in their favor.

Understanding VA Loan Eligibility Requirements

Military service requirements determine VA loan eligibility for different borrower categories:

- Active duty service members qualify after 90 days of continuous service during wartime or 181 days during peacetime

- Veterans must meet minimum service requirements that vary based on service dates and discharge status

- National Guard and Reserve members qualify after six years of service or 90 days of active duty during wartime

VA loan benefits carry forward through multiple uses, allowing eligible borrowers to buy, sell, and purchase again using the same benefit. The Certificate of Eligibility confirms the availability of benefits and can be obtained through online portals or through lender assistance. Some borrowers qualify for restored benefits even after using a previous VA loan.

Surviving spouses may qualify for VA loan benefits under specific circumstances. Unremarried spouses of service members who died in service or from service-connected disabilities can access these home loan programs. This benefit provides critical housing assistance for military families facing difficult circumstances.

Refinancing Your VA Loan in Today's Rate Environment

Current mortgage market conditions create significant refinancing opportunities for existing VA loan holders seeking better terms. The Interest Rate Reduction Refinance Loan program offers streamlined processing for borrowers seeking lower monthly payments. These refinance loans require minimal documentation and often close faster than traditional refinancing options available through conventional lenders.

Cash-out refinance options allow borrowers to access home equity while potentially securing better loan terms and rates. VA cash-out refinance loans can replace existing VA or conventional mortgages while providing cash for home improvements, debt consolidation, or other financial needs. Current rates determine whether cash-out refinancing makes economic sense for individual borrowers.

Refinance loan timing depends on rate differences, closing costs, and long-term housing plans for military families. Generally, refinancing becomes worthwhile when new rates are at least 0.5-1% lower than current loan rates. However, VA refinance loans often justify more minor rate differences due to reduced fees and streamlined processing requirements.

Calculating Refinance Benefits

Understanding refinance math helps borrowers make informed decisions about loan changes:

Monthly payment reduction provides an immediate improvement in cash flow when rates drop significantly, enhancing the overall affordability of the mortgage loan.

- Total interest savings over the life of the loan can amount to thousands of dollars with favorable rate changes.

- Break-even analysis determines how long it takes for closing cost savings to offset upfront expenses.

IRRRL loans typically require lower closing costs than conventional refinancing, making minor rate improvements financially beneficial. These streamlined refinance loans normally bypass many traditional requirements, such as new income verification and property appraisals.

Refinance rates today vary by loan type and borrower qualifications, affecting the overall mortgage experience. Cash-out refinance loans generally carry slightly higher rates than rate-and-term refinancing options. Shopping multiple lenders helps borrowers compare offers and secure the best available terms for their specific situation.

Shopping for the Best VA Mortgage Rates and Lenders

Different lenders offer varying VA loan rates and service levels, making comparison shopping necessary for optimal results and savings. Online mortgage companies often offer competitive rates by reducing overhead costs, while local banks offer personalized service and community expertise. Credit unions frequently provide excellent rates and member-focused service for eligible borrowers with membership access.

Annual percentage rate calculations help compare total loan costs beyond just interest rates, enabling more accurate comparisons. APR includes interest rates plus closing costs, providing a more complete picture of loan affordability over time. However, borrowers should still compare individual fee components to understand actual cost differences between competing lenders.

Lender selection affects both immediate costs and long-term service quality throughout the loan process and beyond, influencing the monthly mortgage payment. Some companies specialize in VA loans and understand military borrower needs better than general mortgage lenders. VA-focused lenders often provide faster processing, better communication, and more flexible underwriting approaches for service members.

Rate lock timing protects approved borrowers from market volatility during loan processing. Most lenders offer 30-60-day locks at no cost, with longer periods available for a loan origination fee. Understanding lock policies helps borrowers time their applications and protect favorable rates through closing, ensuring they benefit from lower interest rates.

Preparing for the VA Loan Application Process

Strong loan applications improve rate offers and approval chances:

- Gather complete financial documentation, including pay stubs, tax returns, and bank statements

- Review credit reports for accuracy and address any errors before applying. • Calculate comfortable monthly payment amounts based on total household budget.

Pre-approval letters demonstrate strong buyer intent and help with home-shopping negotiations in competitive markets. These letters also lock in rate quotes for specific periods, protecting borrowers during house-hunting activities. Multiple lender pre-approvals allow rate and service comparisons before final selection and commitment to particular loan terms.

VA loan processing typically takes 30-45 days from application to closing for most borrowers with complete documentation. Borrowers can expedite timelines by providing full documentation promptly and responding quickly to underwriter requests. Experienced VA lenders often close loans faster than companies with limited military lending experience and specialized knowledge.

Maximizing Your VA Loan Benefits for Long-Term Success

VA loan advantages extend beyond initial home purchases, providing ongoing benefits throughout homeownership, including access to lower interest rates. The loan program allows assumable mortgages, enabling future buyers to take over existing loan terms when selling. This feature can provide selling advantages when mortgage rates are higher than existing loan rates.

Property tax and homeowners' insurance requirements remain standard for VA loans, though some counties offer veteran property tax exemptions. Homeowners' insurance costs vary by location and coverage levels, affecting total monthly housing payments beyond principal and interest calculations.

VA loan benefits include protection against foreclosure through special servicing requirements. Lenders must provide additional assistance and workout options before initiating foreclosure proceedings on VA-backed loans. This protection offers important security for borrowers facing temporary financial difficulties.

Building equity through homeownership creates long-term wealth opportunities for military families, particularly when they secure a fixed rate. Property appreciation and loan principal reduction combine to increase net worth over time. VA loans make this wealth-building strategy accessible without requiring large down payments.

Future home purchases remain possible using VA loan benefits multiple times throughout eligible borrowers' lives and military careers. Restored benefits allow repeat usage after selling previous homes, while remaining benefits can fund additional property purchases in some circumstances. Understanding these options helps military families plan long-term housing strategies and maximize their investment opportunities through strategic homeownership decisions.

Connect With Us

Please share – it really helps